When Justin Trudeau became Prime Minister in 2015, he stated his government would incur a “modest short-term deficit” of less than $10 billion in each of its first three years and promised a balanced budget by fiscal 2020. But despite having inherited improving national finances from his Conservative predecessor that were on-track towards a balanced budget in another year or two, Trudeau then ran nine consecutive deficits, the last reaching $61.9 billion in fiscal 2024 – nearly doubling Canada’s accumulated federal debt from $650 billion to $1.24 trillion.

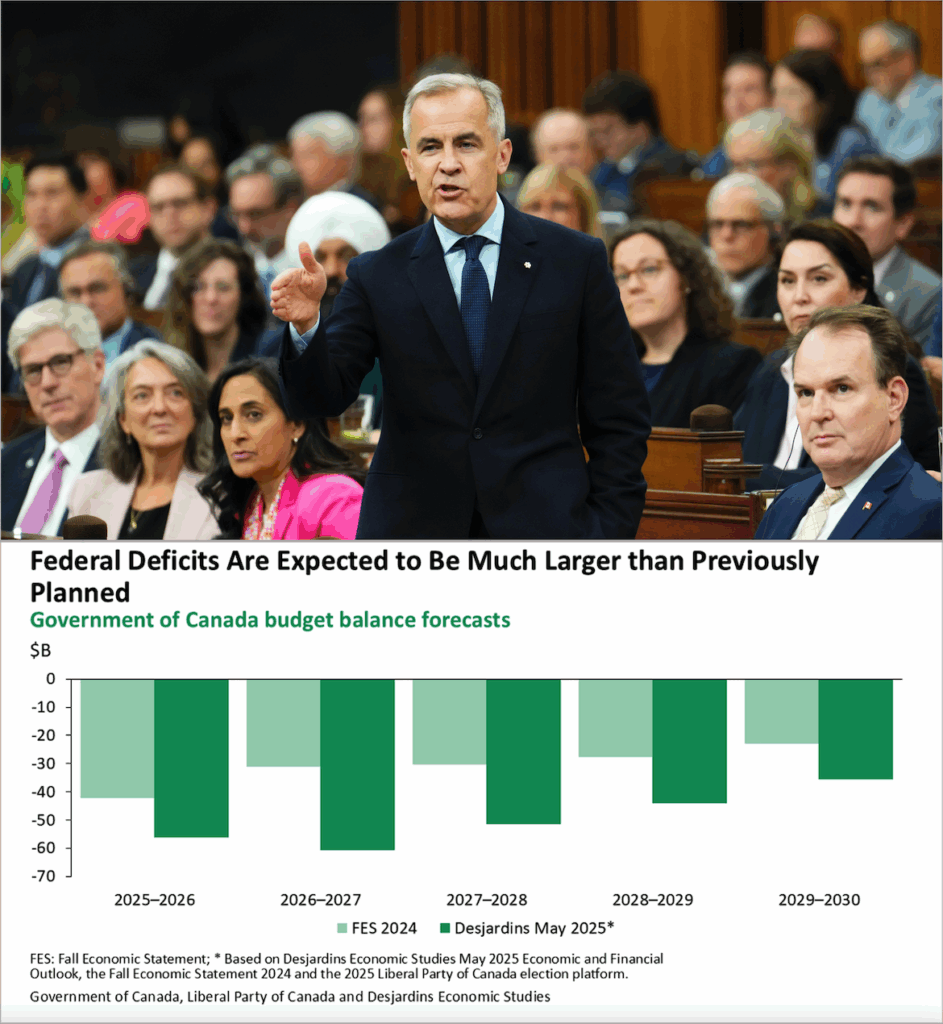

Who could have imagined that a supposedly prudent and ultra-competent former governor of two central banks would make Trudeau look frugal by comparison? The Government of Canada’s recently released spending plan, formally known as the Main Estimates, shows that spending in the fiscal year ended March 31, 2026 will increase by a further 8.5 percent over the current fiscal year to $437.8 billion, plus $74.1 billion in “non-budgetary spending” such as EI payouts, plus at least $49 billion to service the burgeoning national debt. After a couple of other calculations peculiar to the Main Estimates, this yields total planned expenditures of $554.5 billion during Mark Carney’s first year in office.

Even if tax revenues were to remain level with last year, that implies a $40 billion deficit. But given the tariff wars ravaging Canada’s automobile, metals, appliances and consumer goods sectors, the Carney government is facing an all-but certain decline in revenue. Further increasing public spending in the face of these realties will surely result in a record-setting deficit easily exceeding 3 percent of Canada’s GDP and thus dwarfing our meagre annual economic growth.

During Trudeau’s time in office, the Canadian dollar’s foreign exchange value fell from US$0.77 to US$0.696 on January 6, 2025 – the day he finally resigned as Prime Minister. To signal that his departure heralded a new era of fiscal responsibility, much was then made of Carney’s directives that federal departments look for savings and trim staff. But amidst Canada’s daunting financial challenges, such marginal measures are utterly trivial – if they are being implemented at all. Carney’s stunning plan now to actually increase spending will both accelerate inflation and push the international value of our currency down once more.

In a recent article entitled “Mark Carney Was Right: He’s Not Justin Trudeau. He Spends More”, Franco Terrazzano of the Canadian Taxpayers Federation points out that Carney’s intensification of Trudeau’s debt-fuelled spending spree will raise interest costs precipitously. “The Main Estimates say that this year the government will spend $49 billion on interest [and] the Parliamentary Budget Officer projects interest charges blowing a $70-billion hole in the budget by 2029,” Terrazzano warns. “This spending spree means Canadians’ kids and grandkids will be making payments on Ottawa’s debt for the rest of their lives.”

That brings us to the matter of our country’s credit rating. A nation’s credit rating is vital both for accessing capital markets and determining the interest rate paid; it also carries powerful symbolic value that influences investors’ opinion about a country’s overall economy and investment climate. A recent report by New York-based credit rating firm Fitch Ratings, Inc. provides a warning. “Canada has experienced rapid and steep fiscal deterioration, driven by a sharply weaker economic outlook and increased government spending during the [recent] electoral cycle,” the report states. “If the Liberal program is implemented, higher deficits are likely to increase federal, provincial and local debt to above 90% of GDP.” Although Fitch didn’t yet downgrade its rating for Canada, the firm’s message is clear.

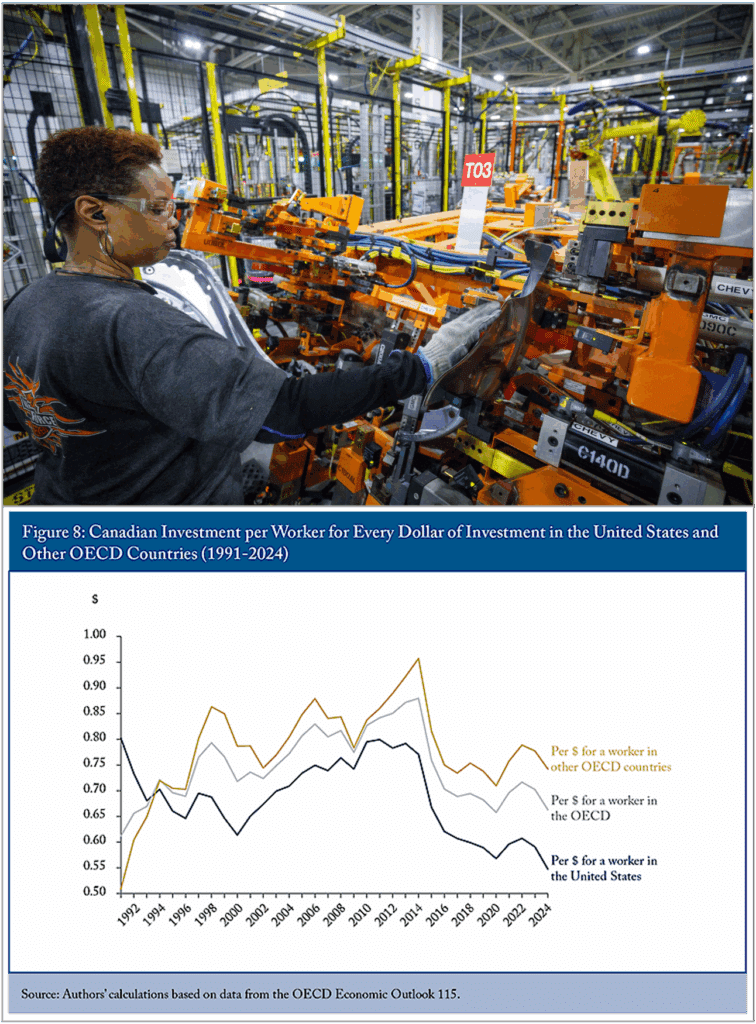

Canadian voters need to stop looking “south” for an easy explanation and – a scapegoat – for our nation’s woes. The Canadian economy was in deep trouble long before Donald Trump’s tariff wars. Business investment per worker is a key predictor of a nation’s evolving productivity and, ultimately, its overall standard of living. “Capital available per Canadian worker has been shrinking since 2015,” warns a recent C.D. Howe Institute media release. Headlined “Canada’s Capital Crisis: The Growing Threat of Falling Business Investment to Productivity”, it continues: “When businesses invest, they equip workers with better tools, driving productivity and, in turn, higher earnings and improved living standards. The fact that Canadian workers are increasingly underequipped compared to their peers abroad signals less competitiveness and lower wages – a threat to our quality of life.”

Who was the real saviour? Some credit Carney – including Carney himself – for steering the country through the 2008 financial crisis while he was Bank of Canada Governor; in fact, Conservative Prime Minister Stephen Harper and his Finance Minister, Jim Flaherty, made the key decisions. Shown at left, Harper (right) with Flaherty about to deliver the 2008 budget speech. (Sources of photos: (left) The Canadian Press/Sean Kilpatrick; (right) Financial Times)

Who was the real saviour? Some credit Carney – including Carney himself – for steering the country through the 2008 financial crisis while he was Bank of Canada Governor; in fact, Conservative Prime Minister Stephen Harper and his Finance Minister, Jim Flaherty, made the key decisions. Shown at left, Harper (right) with Flaherty about to deliver the 2008 budget speech. (Sources of photos: (left) The Canadian Press/Sean Kilpatrick; (right) Financial Times)Then last week, Carney upped the ante by almost unbelievably pledging that Canada would match the new NATO spending target of 5 percent of GDP. If he and his Liberal colleagues follow through, Canada’s defence spending will balloon to the current annual equivalent of $155 billion. This is utterly unaffordable, obviously, and in my view is more revelatory of Carney’s true impulses than any hopes he might govern “sensibly”.

Millions of Canadians were fooled by Mark Carney’s image as the great global banker, the serious and experienced technocrat who could safeguard Canada’s vital interests in going eyeball-to-eyeball against Trump. That image is starting to crack. Instead of respecting Carney, Trump is almost toying with him, last Friday announcing on social media that the U.S. was pulling out of the much-ballyhooed bilateral trade talks launched at the G7 Summit less than two weeks earlier – and brusquely adding that Carney would find out the new tariff rates on Canadian goods in the following seven days.