Feeling comfy? Despite the friendly claims of bank ads, the banks’ actions during the Emergencies Act left many customers feeling uneasy and abandoned.

Feeling comfy? Despite the friendly claims of bank ads, the banks’ actions during the Emergencies Act left many customers feeling uneasy and abandoned.

During the ten days that the Emergencies Act was in force, the banks went out of their way to serve Ottawa’s best interests. And in doing so turned their backs on those very customers they claim to love so much. That green chair doesn’t look quite so comfy anymore.

How Canadians’ Accounts were Frozen – the Emergencies Act Hearings

Mason’s appearance before the Finance Committee was part of a series of hearings examining the invocation of the Emergencies Act from February 14 to 23. While a fuller story will likely emerge from the upcoming federal judicial inquiry, the committee hearings offered an early fact-check on many of the wilder accusations hurled at the 24-day-long truckers’ freedom protest in Ottawa.

That hysterical CBC claim that foreign money – quite likely Russian – was behind the protest? A representative of the crowdfunding site GoFundMe informed the committee that 86 percent of the donors and 88 percent of the funds donated were Canadian. Accusations that the Emergencies Act was necessary to activate an expansion of anti-terrorist funding legislation due to the nefarious intent of the protest’s supporters? Barry MacKillop, Deputy Director of Intelligence for the FINTRAC, the federal body that tracks suspicious money flows, said terrorism was never an issue. Most donors were simply upset with Covid-19 restrictions, MacKillop said, “And just wanted to support the cause by giving small amounts of money. It was their own money…I don’t believe that they thought that they were funding terrorist activity.”

RoseAnne Archibald, National Chief of the Assembly of First Nations, used her appearance before the committee to express concern about the innovative use of financial sanctions against the protesters which, she feared, could set a precedent for how future native protests are dealt with. “I am concerned about the federal government’s increased ability to interfere with the business of crowdfunding websites,” Archibald said. “First Nations have used these crowdfunding websites, for example, to raise legal defence funds.” She added, “I’m equally troubled by the ability of Canadian financial institutions to temporarily and selectively cease to provide financial services to specific clients.” She’s not alone.

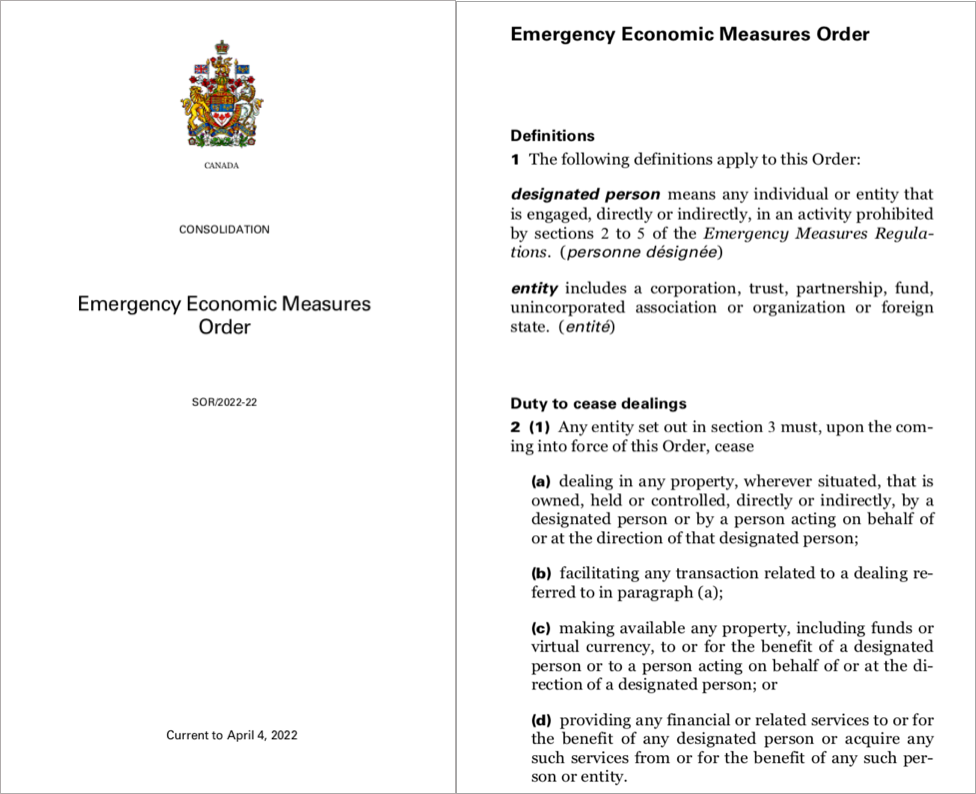

The committee spent a lot of its time studying the complicated and often puzzling details regarding how the bank accounts of protest supporters came to be frozen. Under the Emergency Economic Measures Order issued by the federal government on February 15, Canadian banks and other financial institutions were compelled to cease all dealings with individuals “engaged, directly or indirectly, in an activity” deemed illegal by the Emergencies Act. Anyone associated with the protest was thus at risk of finding their bank accounts and other financial lifelines instantly put beyond reach – and, under the order’s breathtakingly broad scope, so might anyone trying to help out someone whose bank account had been frozen. For how long, nobody could say, nor how a frozen account could be “unfrozen,” or whether this would entail fees and fines or other losses.

Mason explained the technical process: “Upon receipt of information from the RCMP regarding individuals and entities engaged in conduct or activities prohibited under the regulations, banks acted in accordance with their legal requirements under the order.” Given a list of names by the RCMP, the banks basically checked to see if anyone on it was a customer of theirs and if their transactions corresponded with police allegations. If so, their accounts were frozen.

The RCMP says at least 257 accounts, including personal, business and mutual fund holdings, plus 170 Bitcoin wallets, were blocked in this way. Given the expansive manner in which the powers were explained in the emergency order, however, it could just as well have been thousands of accounts that were frozen. Anyone who gave even $20 to the Freedom Convoy through one of several crowdfunding platforms could have been captured by such a sweeping order. And the consequences for those who had their accounts frozen could be devastating, even if short-lived.

Having one’s bank accounts frozen goes far beyond being unable to grab some cash for a night out. Such a person is – suddenly and without warning or recourse – unable to pay any bills. Automated payments and withdrawals cease. A person could default on their mortgage or car payment, or fail to pay a critical utility bill in the middle of a Canadian winter. If such a person was the proprietor of an unincorporated business, their suppliers, contractors or employees would go unpaid. If travelling far from home, they might be stranded at a remote gas station or in another country. The targets of such government action are effectively rendered outcasts from our modern and increasingly cash-less economy.

“You cannot function in society today without financial services,” agrees Conservative MP Adam Chambers, a member of the Finance Committee. “You can’t pay your bills. You can’t buy groceries. Losing access to banking services has very, very serious consequences.” Understanding and controlling the operation of this powerful new sanction is crucial to a functioning democracy, Chambers warns. “We are setting the precedent for how the Emergencies Act will be used in the future.”

Frozen Finger-Pointing

The most unsettling aspect of this new precedent is the lack of honesty about who held the real power to freeze the accounts. In his testimony before the Finance Committee, Michel Arcand, RCMP Assistant Commissioner, Federal Policing Criminal Operations, said, “The RCMP worked closely with municipal and provincial partners to collect relevant information with regard to persons, vehicles and companies directly or indirectly involved in the prohibited and illegal activities…who did not want to leave downtown Ottawa.” Beyond not wanting to leave Canada’s beautiful capital city, the Mounties have not explained what else might trigger an appearance on their fateful list.

And despite the RCMP’s sole discretion in putting names on the list, Arcand went to great effort to downplay the list’s significance and shift focus onto the banks’ use of it. The Emergency Economic Measures Order, he said, “gave financial institutions the ability to freeze financial products of individuals and companies suspected of involvement in prohibited activities during the public emergency.” [Emphasis added.]. To hear the RCMP tell it, they just offered up a spreadsheet of suggested names and the banks took it from there.

That’s not how the banks saw it. When asked by committee members if it was possible to refuse to freeze an account of someone whose name appeared on the RCMP’s list, Mason said she was unaware of any CBA member that did so. Pressed further, she admitted it would have been “very challenging to dispute what the RCMP had provided us with.” It was, she averred, “a legal obligation” to freeze every account on the list.

“None of the financial institutions believed they had the discretion to say no” to the RCMP’s list, observes Chambers in an interview. “They all believed they were under a legal obligation when provided with a name.” Such a situation, he says, amounts to an outsourcing of the federal judicial system, since it essentially made the banking sector “the judge, jury and executioner” of Ottawa’s trucker-protest enforcement policy.

The Requirements of “Due Process”

The flaccid assertion that it was the banks, not the RCMP, who properly decided which accounts to freeze is a legal fig leaf meant to maintain the ruse that the Canadian Charter of Rights and Freedoms was in effect throughout the Emergencies Act’s use. As private entities, banks can choose to lock-down a customer’s account based on their own internal risk assessments without affecting anyone’s Charter rights. Governments, on the other hand, need a court order to impose such a sanction on a citizen. It’s called due process.

Following due process may be inconvenient and time-consuming for a government panicked about a raucous trucker protest. But it is certainly not impossible. As Bloc Québécois MP Gabriel Ste-Marie noted during the committee hearings, five days before the Emergencies Act was invoked, the Ontario government obtained a court order freezing the accounts of two Freedom Convoy crowdfunding sites on the GiveSendGo platform.

Straight to the nuclear option: Bloc MP Gabriel Ste-Marie noted that the Ontario government obtained a court order to freeze accounts connected to the truckers’ protest; why did the federal government think it necessary to unleash the extraordinary powers of the Emergencies Act to achieve the same thing?

Straight to the nuclear option: Bloc MP Gabriel Ste-Marie noted that the Ontario government obtained a court order to freeze accounts connected to the truckers’ protest; why did the federal government think it necessary to unleash the extraordinary powers of the Emergencies Act to achieve the same thing?

The issues pile up. The committee heard there was no process to inform people their accounts had been frozen. They were expected to figure it out on their own, when their credit card was refused at a store, for example. And the lack of direction regarding what should be done with all the personal information that was distributed throughout the financial services industry after the order was rescinded raises significant questions of privacy, adds MP Chambers. Having one’s name on the RCMP’s list may prove to be a lifelong black mark for those targeted, he worries.

The federal government was clearly hasty and slipshod in going after supporters of the trucker protest. The policy was neither well-thought out nor legally iron-clad. This can likely be ascribed to the prime minister’s eagerness to politicize the event, and his rush in trying to bring it to a quick conclusion. The bigger question is why the banks would go along with a scheme that made them the tip of the government’s spear. Not every industry is prepared to toss their customers’ interests aside so quickly.

Standing Up for Customers’ Rights: the “Tower Dump” Case

The banks’ quiet acceptance of federal demands during the Emergencies Act contrasts sharply with how the telecom industry reacted when faced with a similar law enforcement demand. In 2014, police in Peel Region, a sprawling municipality in the Greater Toronto Area, told wireless providers Rogers and Telus to hand over a massive set of data collected from dozens of cell phone towers throughout the municipality. This was a shot-in-the-dark attempt by police at solving a puzzling rash of jewelry store robberies. Bereft of other ideas, they figured they might be able to spot the culprits by sifting through the cell phone data of literally everyone who was ever in the area during the heists.

While both companies dutifully responded to thousands of individual cell phone record production orders prior to 2014, the Peel Region “tower dump” order was so different in scope – entailing detailed information on over 43,000 law-abiding customers – that they felt compelled to challenge its legality on constitutional grounds. And while the police eventually thought the better of their request and withdrew the production order, Rogers and Telus pressed on with their case to establish a legal precedent on behalf of their clients. They also announced they would henceforth demand a warrant before sharing any basic customer information with police or security agencies.

In his 2016 ruling on the case, Ontario Superior Court Justice John Sproat handed an unequivocal victory to the telecoms – and, by extension, to their customers. First, Judge Sproat dismissed arguments that the two companies lacked standing to take their customers’ privacy concerns to court. He ruled, in fact, that the firms were likely the only parties able to effectively defend such rights in the face of government overreach, as “no individual subscriber would have an interest in litigating with the government over these issues.”

As for the substance of the matter, Sproat declared the original production order “overly broad and unconstitutional” and laid out new standards to constrain future data fishing expeditions by police. It was a clear win for Canadian citizens concerned about their privacy rights. But it was a legal victory made possible only because private businesses were prepared to stand up for their customers.

And the two firms involved made it clear they’d do it again, as often as necessary. “As we have done in this case, Telus, will contest orders we believe overreach in order to protect the privacy rights of our customers and other Canadians,” the firm said in a media release. Rogers said essentially the same thing, “We thought the request we received was too broad, so in order to protect our customers’ privacy, we went to court to seek clarification.” Whatever you might think about Canada’s cosseted and expensive cell phone industry, Telus and Rogers spent their own resources in a principled defense of their customers’ rights.

What happened when the banks found themselves in the same squeeze? They embarrassed themselves with a lack of gumption and principles. All the more damning is the fact they had advance notice. “We were given a head’s up that [the Emergencies Act] was coming,” Mason admitted to the Finance Committee. So, the banks knew they were about to be hit with a government demand that they freeze their customers’ accounts in the absence of a court order. And they still chose to do nothing.

“Any of the banks could have challenged the lawfulness of the order made pursuant to the Emergencies Act, and applied for an injunction pending the hearing of the case,” says Queen’s University law professor Bruce Pardy. There’s no guarantee such a last-minute challenge would have succeeded, he admits. “But at least it would have sent a signal that they regarded their customers’ interests as sacrosanct and objected to being strong-armed by the government.” Doing so would have also laid bare the federal government’s role and intentions in this entire matter.

No Big Deal, or Millions in Panicked Withdrawals? The Credit Unions Speak Out

Since the Emergencies Act was revoked on February 23, the banks have avoided publicly criticizing the federal government’s actions. In fact, CBA testimony at the Finance Committee significantly downplayed the impact of the order on the banks’ customers. When asked how the freeze orders affected account holders, Mason lamely said that, “there has not been anything of concern.” Colleague Darren Hannah, the CBA’s Vice-President Finance, Risk and Prudential Policy, added, “We didn’t really see a material change.” Freezing bank accounts on demand? No big deal. Not “material,” anyway.

Such a blasé response conflicts sharply with that of Martha Durdin, president and CEO of the Canadian Credit Union Association. During her appearance Durdin told the Finance Committee that, “Many of our members expressed…concern” about the freeze order, that “there was some degree of panic,” and that “Many Canadians made significant withdrawals from credit unions as a result, sometimes in the hundreds of thousands of dollars, and a few occasions millions.”

One credit union leader, Durdin said, wrote to the association saying that, “We had a tremendous amount of members very seriously concerned regarding the government’s ability to seize accounts; it brought forward a large sense of mistrust with the government.” (Durdin also noted that her organization wasn’t given the same “head’s up” about the looming invocation of the Emergencies Act as her competitors at the banks said they were.)

What explains this apparent difference in attitude between customers of banks and credit unions? It is possible that members of credit unions, which operate on a cooperative basis and share their profits with member-depositors, are categorically different from bank customers, and therefore reacted to the freeze order in an entirely different way. Credit union membership tends to skew rural and members may place a greater value on personal independence and be innately more suspicious of government. It is probably also significant that credit unions are regulated primarily at the provincial level, are far smaller than the chartered banks, are locally or regionally managed, and have always made close ties to their community central to their branding.

Then again, many credit unions are based in large cities and collectively have millions of urban members who regard banks and credit unions as basically equivalent financial service providers in competition with one another. It thus seems highly curious that bank customers would not have had worries similar to their credit union compatriots that their financial accounts could be frozen at a whim. Far more likely is that bank customers were equally outraged by such a scenario, but that the banking industry chose to downplay these complaints. That would certainly align with the banks’ overall pliancy regarding government policy during the trucker crisis.

Don’t forget about your customers: The Emergencies Act has focused new attention on substantial differences between banks and credit unions; pictured, a pointed ad campaign by the Edmonton-based credit union Servus.

Don’t forget about your customers: The Emergencies Act has focused new attention on substantial differences between banks and credit unions; pictured, a pointed ad campaign by the Edmonton-based credit union Servus.

The tight connection between the banks and Ottawa is reflected in the industry’s prodigious lobbying efforts. According to the most recent records from the Office of the Commissioner of Lobbying of Canada, the CBA engaged in 30 separate communications with federal officials or employees over the past six months and employs a registered lobbying staff of 27. Plus, each individual chartered bank has its own lobbying arm, which is often nearly as big as the CBA’s. Scotiabank, for example, had 17 communications with government over the past six months and lists 18 lobbyists; Royal Bank had 11 interactions and has 13 registered lobbyists. By comparison, the Dairy Farmers of Canada – another heavily-regulated group whose financial wellbeing depends on the maintenance of those regulations – had 47 communications with the federal government and 13 designated lobbyists during this time.

Unlike the dairy sector, however, the banking industry has never been able to bend Ottawa completely to its will. Recall, for example, the failed bank merger efforts of the early 2000s. Despite its size and lobbying efforts, the banking sector suffers from a curious lack of political clout. They may be extremely successful, but few people really care about the banks. And because of this, the sector may have decided that the benefits of obedience outweigh the risks of exhibiting the kind of independence and feistiness it displayed prior to the merger-proposal era. Those fat profits keep rolling in, but the banking industry appears to have forgotten whose interests it is supposed to be serving, and where those profits actually come from.

Unfortunately, this comprehensive capture by the federal government has left the banks vulnerable to a steady stream of additional burdens and demands that also can’t be refused. We might consider this the fate of any “kept” industry. In addition to being forced to implement the Trudeau government’s vendetta against the truckers’ protest, for example, the banks have also been handed a bill for its profligate spending habits.

Thanks for helping out, suckers! After dutifully serving the Trudeau government during the Emergencies Act, the banks were later “rewarded” with an extra $6 billion in new federal taxes over the next five years, including a special higher corporate tax rate of 16.5 percent. (Source of photo: Shutterstock)

Thanks for helping out, suckers! After dutifully serving the Trudeau government during the Emergencies Act, the banks were later “rewarded” with an extra $6 billion in new federal taxes over the next five years, including a special higher corporate tax rate of 16.5 percent. (Source of photo: Shutterstock)