Alberta boasts many distinct advantages. There are the awe-inspiring, sky-blocking mountain views of Banff, Jasper and Waterton national parks. An embarrassment of energy resources is another obvious advantage. As was, for a time in the 1980s, the presence of two sports legends – Wayne Gretzky and Mark Messier – on the same Edmonton Oilers hockey team. And don’t forget the tremendous demographic advantage of having the country’s youngest and most dynamic population.

But there was only ever one double-uppercase “Alberta Advantage”. Beginning in the 1990s under Progressive Conservative premier Ralph Klein, the province marketed itself across Canada and around the world as a low-tax haven based on three key factors. First, the province had no provincial sales tax. Second, it maintained by far the lowest corporate taxes in Canada. Third, instead of a productivity-inhibiting progressive personal income tax, it levied a unique flat tax of 10 percent on all earned income.

These three tax policies made Alberta the most attractive province in the country for wage earners and investors alike. In combination with a booming oil and natural gas sector, the Alberta Advantage also raised the province’s reputation globally. As a result, it often beat out not only other provinces but even low-tax U.S. states such as Texas and North Dakota for job creation and investment. As both fiscal policy and branding exercise, the Alberta Advantage was phenomenally successful. And the key to this reputation was its flat income tax – a revolutionary move meant to signal the government’s intent to keep out of the way of hard-working taxpayers.

Eventually, however, the good times faded. The oil boom gave way to bust. U.S. states – and some provinces – responded with their own tax reductions. And political upheaval and incompetence within Alberta eroded what was once the province’s clear tax lead. Today the flat tax is long gone, replaced with the same sort of progressive rate structure as every other province. Corporate tax rates were hiked to levels comparable to other provinces, then dropped again, leaving an overall advantage that’s less certain than it once was. And while there’s still no provincial sales tax, an unending chorus of elite opinion constantly demands its imposition, raising the political risks that this tax advantage might disappear one day as well.

What can Alberta do to get its Advantage™ back?

The Alberta Advantage Origin Story

Klein came to power in 1992 facing a massive fiscal crisis left by his predecessor Don Getty, whose government had spent freely to diversify the Alberta economy away from oil and gas through large-scale government investment in such things as cellphone manufacturing, paper mills and magnesium smelting. Tackling the overspending problem head-on, Klein slashed across the board while also keeping taxes low. Per capita government outlays fell by more than $3,000 in his first four years as premier – from $11,000 in 1992-93 to $7,450 in 1996-97.

Along with spending much less, Klein and key ministers such as Treasurer Jim Dinning and Municipal Affairs Minister Steve West set about eliminating needless government regulations while simplifying and speeding the approval process for businesses and major projects, signalling both in rhetoric and substance that Alberta was “open for business”. The combination of low taxes, fiscal responsibility and deregulation proved stunningly successful, so much so that by 1999, Klein’s government could boast, “Lord willing, in the year 2000, Alberta will have not only a balanced budget and the lowest overall taxes in Canada, but also a net debt of zero.” The Alberta Advantage was born.

Once the deficit had been tamed, the Klein government shifted its focus to cementing these benefits by effecting a permanent and dramatic change in the income tax system. The prime mover in this process was Stockwell Day, who succeeded Dinning as treasurer in 1997. An ideological conservative, Day was drawn to the idea of reforming the tax system in a way that would both spur growth and keep a lid on future government spending.

His solution was a flat, or single-rate, personal income tax that that would treat all taxpayers equally. “We believed that a single-rate tax would not only encourage productivity but would also put up guardrails to prevent government from over-expanding,” Day recalls during an interview from his home in Kelowna, B.C. (Following his time in provincial politics, Day represented the area as an MP from 2000 to 2011, serving as both leader of the federal Canadian Alliance Party and later as a cabinet minister in the Conservative government of Prime Minister Stephen Harper.)

For Day, the flat tax was more than academic theory, it was visceral. “A progressive tax system is inherently anti-productive,” he asserts. “It discourages extra effort and innovation because people know that working harder or earning more means getting taxed at a higher rate.” The future minister had firsthand experience with this productivity-dampening effect. “When I was younger, I worked in a [meat] packing plant,” Day says. “My colleagues would often refuse overtime because they believed the extra effort wasn’t worth it as their overtime would just be taxed away at a higher rate” if the additional income moved them into a higher bracket. “That always stuck with me. Why punish people who want to work harder?”

With a single or flat-rate tax, working harder does not mean losing more of one’s earnings to taxes. Due to the fact he or she makes more, a higher earner will naturally pay more taxes than a low earner in absolute terms. But no one has to pay a greater or lesser share of what they earn. This makes a flat tax both fair and simple to administer. But Day believed a flat tax held more than just economic appeal. It could also serve as a sign that Alberta was different from other jurisdictions, where the income tax rate rises with income.

The political message embedded in the flat tax was two-fold, he says. First, it was an inducement to move to Alberta, where “hard work would be rewarded, not penalized.” Second, it signalled to voters that Alberta was serious about keeping a lid on future tax increases. This is because it is common for campaigning politicians to promote incremental tax changes by arguing that the increase will only affect “other” voters – most often anyone wealthier than the current audience. But while claims that “only the rich will pay” may seem comforting to many, over time such changes have a habit of ensnaring all taxpayers, either via inflation or by an expansion in tax brackets or other mechanisms.

With a single or flat rate, such an argument is moot. Any income tax change will necessarily affect all taxpayers equally and at the same time. This embedded equality factor, Day argues, was the secret means to quench what he calls “the insatiable thirst of government to grow.”

A Fiscal Revolution

To evaluate and fully discuss Day’s flat tax concept, Klein’s government struck a Tax Review Commission, chaired by respected businessman Jack Donald (founder of the Fas Gas chain of gas stations). The commission consulted widely with Albertans and concluded that the province should stop calculating personal taxes as a percentage of federal taxes (which are steeply progressive) and move instead to a stand-alone provincial “tax on income” approach using a single rate. This was implemented via a three-year plan unveiled in 1999 that promised to “blaze a new trail across the taxation frontier, becoming the first to move to a simple, single rate of tax on income.”

The new rate was to be set at 11 percent. Day had his revolution. Simultaneously, the personal income tax exemption was raised by 60 percent and the spousal income exemption doubled, thus levelling the playing field for one-income families. The overall goal, Day stated at the time, was to ensure that “all Albertans at all levels will pay less in taxes.”

A popular revolution: With the flat tax in place and the economy surging, Klein’s Progressive Conservative party won a landslide re-election victory in the 2001 election, capturing a majority of seats in left-leaning Edmonton for the first time in almost two decades. (Sources: (left image) Calgary Herald; (right photo) CP Photo/Jeff McIntosh)

A popular revolution: With the flat tax in place and the economy surging, Klein’s Progressive Conservative party won a landslide re-election victory in the 2001 election, capturing a majority of seats in left-leaning Edmonton for the first time in almost two decades. (Sources: (left image) Calgary Herald; (right photo) CP Photo/Jeff McIntosh)

A fine balance: Alberta’s Fiscal Responsibility Act demanded budgets be balanced and any surplus directed to debt repayment; in July 2004, Klein famously announced that the province was debt-free – a beacon of fiscal probity in a nation of provincial red ink. (Source of photo: CP Photo/Jeff McIntosh)

A fine balance: Alberta’s Fiscal Responsibility Act demanded budgets be balanced and any surplus directed to debt repayment; in July 2004, Klein famously announced that the province was debt-free – a beacon of fiscal probity in a nation of provincial red ink. (Source of photo: CP Photo/Jeff McIntosh)

That was precisely the plan, says Day. “You want to be competitive, not just within your own national boundaries, but internationally.” Many U.S. companies began to see Alberta as a viable alternative to Texas or North Dakota for expansion, with Alberta attracting tens of billions of dollars in capital investment in energy, finance, real estate and tech startups. By 2006 Alberta’s jobless rate had bottomed out at 3.1 percent, the lowest in three decades. An unprecedented influx of people provided further evidence of economic strength. “We saw a brain drain from other provinces into Alberta,” Day recounts today. The reason? “People knew they could keep more of what they earned, and that was a powerful incentive.”

Together with his tax reforms, Day had also introduced the Fiscal Responsibility Act in 2000 to require that the current budget always be in balance and any surplus funds be saved or directed to debt repayment. The intent, he says today, was to prevent future governments from losing their focus in the midst of a boom. Rather than allowing politicians who came after him to simply spend unexpected oil and natural gas royalties or other forms of new revenue on political goodies, Day wanted to ensure such unintended surpluses were directed to the benefit of future taxpayers. The Fiscal Responsibility Act “made it more difficult to go back on your promise,” he says. In essence, it was a commitment that future governments would be required to live within their means, regardless of booms or busts. That same year, Day left provincial politics to join the federal Reform Party.

The Fall of the Flat Tax

Nothing in politics occurs within a vacuum. The tremendous success of Alberta’s corporate and income tax moves eventually provoked competitive responses from other provinces and states. Saskatchewan and Ontario, for example, significantly lowered their corporate tax rates. Inspired by the simpler Alberta model, Saskatchewan introduced a “simple, three rate ‘tax-on-income’ structure” for its personal income tax system in its 2000-2001 budget.

Following Klein’s retirement in 2006, however, successive PC premiers Ed Stelmach, Alison Redford and Jim Prentice revealed in turn how each lacked their predecessor’s passion for low taxes and limited government. The post-Klein era became notable for a massive expansion of Alberta’s public sector in both size and scale, as public sector union wages soared. There was no “quenching” its thirst to grow, as Day had once hoped. Alberta ran its first post-Klein deficit in 2008-2009, and with it the public debt returned.

According to a Fraser Institute report, between 2005-2006 and 2012-2013, Alberta government spending increases exceeded the rate of inflation plus population growth by over $22 billion, even as oil and natural gas revenues topped out, then plunged severely. Unwilling to face this fiscal challenge with the same decisiveness as Klein had in the 1990s, his successors chose instead to keep spending. In doing so, they repudiated the key tenets of the flat tax and other components of the Alberta Advantage.

The beginning of the end of the flat tax came – perhaps ironically, perhaps fittingly – in the final days of the PC era under Prentice. While his short-lived government is remembered mainly for its ill-advised merger with Danielle Smith’s Wild Rose Party, it was equally notable for abandoning the single-rate income tax in an effort to grab more tax revenue. With the provincial public debt at $11.9 billion, Prentice’s 2015 budget proposed to undo Day’s fiscal revolution by adding a second tax increment of 11.5 percent.

The move still stings, says Day. “To tell you the truth, I was heartbroken,” he recalls. “It felt like it was my baby. And Jim Prentice was a friend of mine. I warned him: ‘If you axe the [flat] tax, it will be a signal to a significant core of your voters that you’re sliding back into progressive habits, of not just taxation but other policies as well. If you do that, I think you’ll be toast.’” More of a centrist than Day, Prentice and his party’s “Red Tories” banked their political fortunes on luring back middle-of-the-road voters from a surging NDP.

Prentice’s budget was never implemented; a few months later NDP leader Rachel Notley ended 44 years of Progressive Conservative government in Alberta with a stunning majority victory. Notley quickly dismantled the entire flat tax concept, replacing it with a five-tier structure topping out at 48 percent (including federal taxes). Corporate taxes were also quickly hiked. RIP Alberta Advantage. Tragically, Prentice himself was killed a year after the 2015 election when the light aircraft he was travelling in crashed.

Progressive habits: After ending 44 years of Progressive Conservative government in Alberta, NDP leader Rachel Notley dismantled the flat tax concept and brought in a five-tier structure. (Graphic by C2C Journal)

Progressive habits: After ending 44 years of Progressive Conservative government in Alberta, NDP leader Rachel Notley dismantled the flat tax concept and brought in a five-tier structure. (Graphic by C2C Journal)Alberta’s Never-ending Sales Tax Debate

Further encroaching upon Alberta’s dwindling Advantage was an ever-present debate over its status as a no-provincial-sales-tax zone. As the province’s fiscal woes mounted, several high-profile economists, most notably Trevor Tombe of the University of Calgary, made a campaign out of promoting a provincial sales tax (PST) as the cure-all for Alberta’s ailing budgets. The province’s heavy reliance on volatile energy revenues and income taxes leaves the province vulnerable to budget shortfalls, the logic goes. According to Tombe, a sales tax of 5 percent would smooth out those fluctuations and create a stable tax base.

Some critics today go so far as to claim the good times during the flat-tax era were simply an illusion. “The province relied on high commodity prices to make up for low taxes,” asserts Thomson, who spent 25 years as a columnist for the Edmonton Journal. “When oil prices were booming, the system worked. But when they weren’t, Alberta’s fiscal stability was on shaky ground.” The only solution to this volatility, critics contend, is more taxes.

In 2022 Thomson contributed a chapter to a collection of essays by policy analysts and economists entitled A Sales Tax for Alberta: Why and How. Chapter headings such as “Alberta Sales Tax: An Inevitability and an Opportunity to Reset” and “Join the Sales Tax Parade! PST and the Road to Alberta’s Economic Recovery” convey the book’s boosterish flavour. Thomson’s contribution is called “The Political Suicide Tax” and acknowledges Albertans’ widespread public animosity towards new taxes. Still, he observes that, “Without a PST, Alberta is passing up $7 billion a year in stable, predictable revenue.”

Perhaps surprisingly, even Day admits to the idea’s superficial attraction: “In a perfect world, a consumption tax is your best form of tax since the rich will pay more simply because they buy more stuff.” But, he stresses, “There’s not a lot of purity in politics.” From a practical point of view, Day remains adamantly opposed because a sales tax would remove the fiscal guardrails he worked so hard to install as provincial treasurer.

Giving politicians access to billions of dollars in “stable” new sales tax revenue paves the way for even more spending, Day warns. And that would further undermine the Alberta Advantage. “Once you introduce a PST, you lose that unique edge,” he cautions. With his flat tax gone and provincial corporate taxes no longer standing far out from the crowd, adding on a sales tax as well would make Alberta “just another jurisdiction” in Canada’s high tax landscape, he frets.

A Spending Problem

Day’s lament that Alberta has become just another province is not entirely correct. It remains quite exceptional in one very significant way: it spends far more per capita on government services than any other province. Over the last 25 years, Alberta’s per-person spending has exceeded the 10-province average every single year. In 2022-2023, Alberta’s program spending was $13,570 per person, over $1,200 more than in Ontario, driven by public-sector wages that are among the highest in Canada. This has given rise to concern Alberta faces a “structural deficit”, in that its expenses now exceed its revenues on a permanent basis.

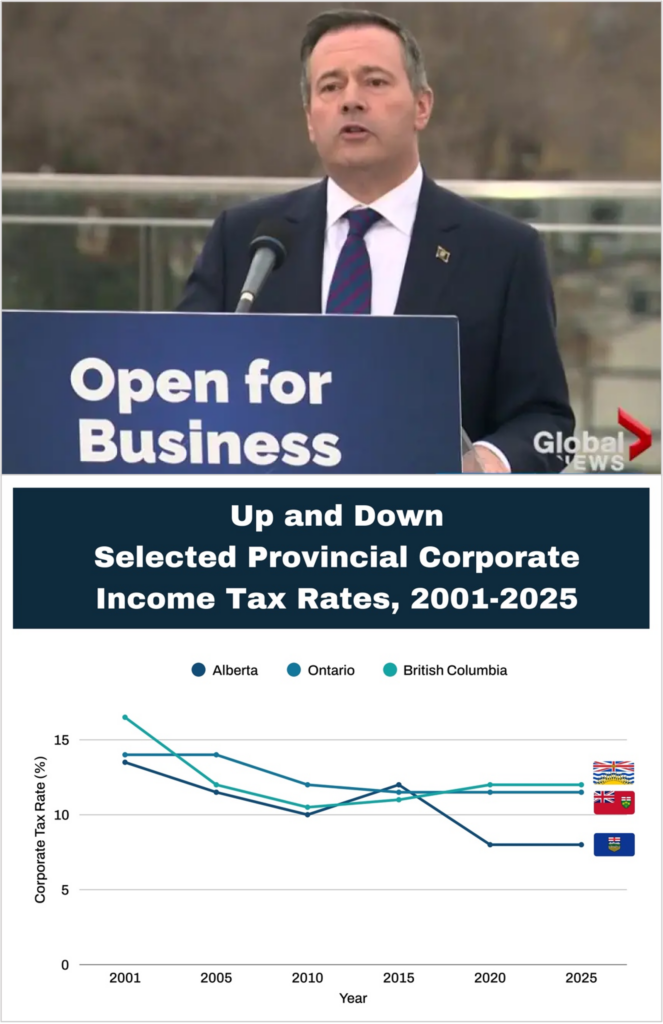

“Open for business” once again: Following the defeat of Notley’s NDP in 2019, the United Conservative Party under Jason Kenney lowered the corporate tax rate from 10 percent to 8 percent and began lifting regulatory burdens on business. (Sources: (photo) Global News; (graph) C2C Journal)

“Open for business” once again: Following the defeat of Notley’s NDP in 2019, the United Conservative Party under Jason Kenney lowered the corporate tax rate from 10 percent to 8 percent and began lifting regulatory burdens on business. (Sources: (photo) Global News; (graph) C2C Journal)

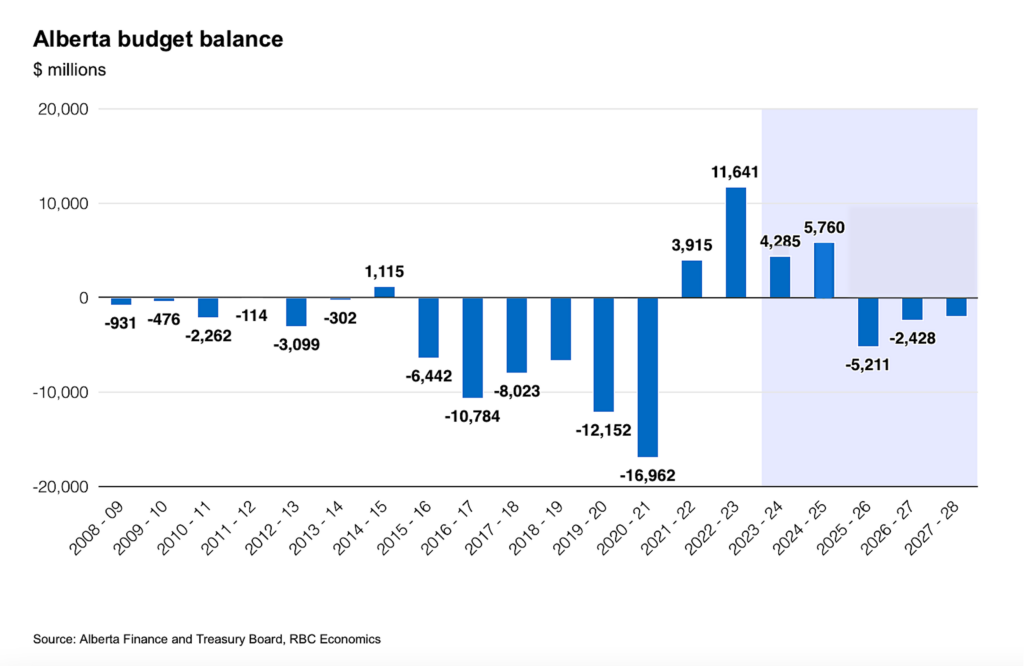

The Kenney government initially tried to trim spending in line with the panel’s advice, but emergency spending during the 2020 Covid-19 pandemic sent the province’s deficit to a record $17 billion. By 2022, another oil boom brought a gusher of revenue and a surprise surplus – and true to historical form, Alberta’s spending shot up again. Now, with oil prices easing, Alberta is in deficit once more. Back and forth it goes.

In 2023, Kenney’s successor Danielle Smith ran on an election platform that included a No Tax Hike Guarantee. “Higher taxes would only serve to stifle economic growth and reduce job opportunities,” Smith said on the campaign trail, promising to actually reduce income taxes. Following some prevarication and delay, the UCP’s most recent budget drops the personal income tax rate on the first $60,000 of income earned to 8 percent, effective January 1 of this year, making it the lowest in Canada.

At the same time, however, Smith raised the education property tax (collected via municipalities) by 6.25 percent. Other hidden tax and fee increases are similarly designed to raise revenues by stealth. And the budget itself incurs a $5.2 billion deficit, with further deficits projected through fiscal 2027, signalling a government still unprepared or unwilling to live within its means. If the UCP government had simply maintained earlier spending plans made during the 2022-2023 fiscal year when the budget was still in balance, it would have posted a small surplus this year. Instead, the net public debt is forecast to hit $43 billion this coming year, and keep growing into the foreseeable future. It’s a long way from Klein’s “Paid in Full” announcement just over two decades ago.

Making matters worse, the Smith government’s effort at replicating Day’s 2000 Fiscal Responsibility Act – the Sustainable Fiscal Planning and Reporting Act – is filled with loopholes, weak benchmarks and sly workarounds, as this lengthy analysis details. The guardrails are essentially gone.

How to Get that Advantage Back

Alberta’s fiscal history over the past two decades shows a clear pattern of ratcheting behaviour: spending climbs during boom years but rarely retreats when revenues fall. A study by University of Alberta economist Ergete Ferede found that for every one dollar increase in natural resource revenue, Alberta’s program spending increased by about 56 cents the following year. In other words, over half of any revenue windfall is quickly baked into future expenditures.

Tax policy in Alberta no longer acts as a clear beacon to the rest of the world that the province is truly a different place. The way it is structured, Smith’s new 8 percent personal income tax bracket actually makes Alberta’s tax system even more progressive than it used to be since the gap between the highest and lowest brackets has now widened. Her latest budget also reinforces the fact that taxes of all sorts can shoot up and down with surprising speed – which will not reassure investors or individuals thinking of moving to Alberta. And the current Sustainable Fiscal Planning and Reporting Act is more sieve than shield, especially when compared to Day’s earlier Fiscal Responsibility Act. The Alberta Advantage ain’t what it used to be.

If the province wishes to reclaim its position as the unquestioned champion of low taxes and limited government, the only sure way to accomplish this is by bringing back Day’s flat tax. A 2023 Fraser Institute report advocates a new 8 percent flat income tax rate – actually lower than Day’s original 10 percent but consistent with the current corporate rate. And since it would apply to all income earners, this move would be categorically different from Smith’s new 8 percent bracket for lower income earners alone.

Such a change – revolutionary in the sense that it would mark a return to the starting point – would once again make Alberta competitive with other oil-producing U.S. states such as Louisiana and North Dakota for job creation, business formation and investment. In fact, Alberta would become the 15th-lowest tax jurisdiction in North America. A restoration of the flat tax, the Fraser Institute report adds, would also “improve tax efficiency, reduce administration and compliance costs, all the while avoiding negative incentives for work, savings and investment.”

But most importantly, the return of the flat tax would announce to the world that future tax hikes are far less likely in Alberta than in any other jurisdiction in the country thanks to its embedded commitment to limited government. Restricting the public sector’s access to new revenues is still the key to quenching the public sector’s thirst to grow. It is also the foundation for re-establishing the province’s once unassailable fiscal leadership. “I would heartily endorse that reconsideration,” Day says of restoring his single-rate tax. “And not just because we put it in place. But because Alberta’s tax advantage is being lost.”

Tade Haghverdian is completing his degree in philosophy, politics and economics at the University of British Columbia. He was previously a student intern at the Alberta Institute and the Institute for Liberal Studies.

Source of main image: Shutterstock.